Funding Pensions

by P

Barber 20 June

2010

Synopsis

1. This paper argues that an adequate fund growth rate is an essential

requirement for the provision of sustainable pensions.

Back Ground

2. The principal behind a pension scheme is that donations are deposited

in a fund during ones working life, and that the combination of these deposits

builds up a fund which is then sufficient to provide an adequate income during

retirement. The critical elements of this process are:

a) the magnitude of the payments deposited in the fund

b) the timing of those deposits

c) the rate of fund growth

d) the rate of inflation

e) the number of years over which the fund is built up

f) the number of

retirement-years that are to be provided

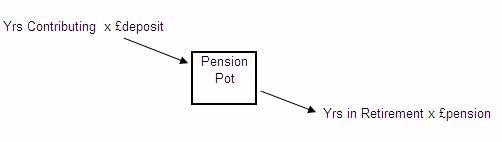

Funding if Growth and Inflation are assumed to be zero

3. If both fund growth and the rate of inflation are

assumed to be zero, then funding becomes a function of:

a) the number of years over which the fund is built up

b) the number of years over which a pension is drawn

4. This process is demonstrated in the diagram below.

5. In the simplified example above it is assumed that

deposits are made in equal amounts throughout the working years and that a fixed

pension is paid for all the years is retirement. It is assumed that the “Pension

Pot” built-up during the working life is the same as the money required to fund

the pension payments.

6. If we now examine this model in terms of Income

percentages the results can be quite alarming. Given that:

a) £deposit = Income x Funding %

b) £pension = Income x Pension Rate%

7. The above process can be defined in terms of the

equation shown below:

Yrs Contributing x Income x

Funding % =

Pension Yrs x

Income x Pension %

8. The pre-1997 standard for a final salary pension fund

was 2/3rds of final pension (i.e. Pension % = 66%), based on forty years

service

9. If the equation above is manipulated and this target

Pension % applied, then the required level of funding can be determined.

Funding % = ( Pension Yrs x Income x 66% ) / Yrs

Contributing x Income

10. Historically a man would have paid into a pension fund

for 40 years, and then drawn a pension for 20 years. Since Income appears both

in the top and bottoms parts of the equation, the required funding % would

be:

Funding % = 20 years x 66\% / 40

years = 33%

11. Needless to say nobody, reaching the age of retirement

today, has funded their pension-pot at a rate of 33% of Income consistently for

the last 40 years. It should be of little surprise therefore that Companies which

still offer final salary schemes are struggling to meet their obligations and

people who are in defined contribution schemes are finding that the pensions at

retirement are an insignificant fraction of the sum they were expecting to

receive when they signed up to join the scheme.

So what went wrong?

12. The key to understanding what went wrong with pension

funding lies with an understanding of the way in which a pension-pot accumulates

interest and dividends on its invested deposits, in addition to the normal

pension-fund contributions. The table below provides an example of the process,

although it should be noted that the process illustrated is quite crude in the

way interest and dividends are calculated, and it also assumes that a single

pension payment of £3,000 is made at the beginning of the year. The process

operates as follows:

i)

in the first year a payment of £3,000 is made into the

fund, this is shown in column b)

ii)

the closing funds, shown in column c) are calculated by

summing the opening balance and the payment into the fund, (£0 + £3,000 =

£3,000)

iii)

at the end of the year interest and dividend is

calculated (in

this case calculated as 10% of the value of the fund) this is shown in column

d)

iv)

the opening funds at the beginning of the second year are

shown in column a), they are calculated by adding the closing balance for the

previous year and the interest and dividends earned in the previous year.

(£3,000 + £300 = £3,300)

|

|

|

Assumed

Growth Rate

= |

10.0% | |

|

|

|

|

|

|

|

|

a) |

b) |

c) |

d) |

|

|

|

|

|

Interest |

|

|

Opening |

payment |

Closing |

&

Dividends |

|

Year |

Funds |

into

fund |

Funds |

earned |

|

1 |

0 |

3,000 |

3,000 |

300 |

|

2 |

3,300 |

3,000 |

6,300 |

630 |

|

3 |

6,930 |

3,000 |

9,930 |

993 |

|

4 |

10,923 |

3,000 |

13,923 |

1,392 |

|

5 |

15,315 |

3,000 |

18,315 |

1,832 |

|

6 |

20,147 |

3,000 |

23,147 |

2,315 |

|

7 |

25,462 |

3,000 |

28,462 |

2,846 |

|

8 |

31,308 |

3,000 |

34,308 |

3,431 |

|

9 |

37,738 |

3,000 |

40,738 |

4,074 |

|

10 |

44,812 |

3,000 |

47,812 |

4,781 |

|

11 |

52,594 |

3,000 |

55,594 |

5,559 |

|

12 |

61,153 |

3,000 |

64,153 |

6,415 |

|

13 |

70,568 |

3,000 |

73,568 |

7,357 |

|

14 |

80,925 |

3,000 |

83,925 |

8,392 |

|

15 |

92,317 |

3,000 |

95,317 |

9,532 |

|

16 |

104,849 |

|

|

|

|

|

|

|

|

|

|

By year

15 we have: |

45,000 |

|

59,849 | |

13. It can be seen that in the table above, by the

beginning of year 16 the funds have built-up to £104,849: of this balance

£45,000 has derived from payments into the fund, while £59,849 has derived from

interest and dividend receipts. It should also be noted that by the end of year

15 the value of interest and dividend payments received at £9,532 is more than

three times greater than the £3,000 contributed to the fund.

14. It is this process of accumulating interest and

dividend payments which was historically the essence of pension scheme funding.

If the above arrangement was to operate for a period of 40 years, then at the

end of the period the value of the fund would be £1,460,555. Which, at a 10%

yield rate would return an income of £146,055 indefinitely; no worries about

living a few years longer with this model. Working the numbers backwards, if the

pension represented 2/3rds of final salary then the final salary would have been

£219,082 (£146,055 x 3 / 2 = £219,082) and the pension contribution rate would

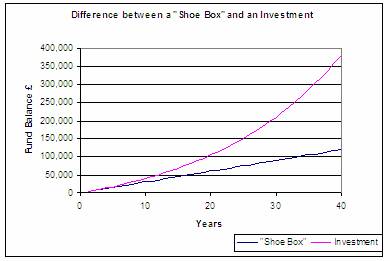

have been 1.36% (£3000/£210,082 = 1.36%). The difference between a fund, which

merely operates as “a shoe box under the bed”, and one which is invested, and

earns a return on the deposits made is illustrated in the graph below.

15. Leaving aside the issue of the “village economy” and as

to whether or not there are sufficient investment opportunities in the “village”

to accommodate this level “collective pension-pot”, the main problem with this

process has been that the interest and dividend rates have been nothing like 10%

over the accumulation period.

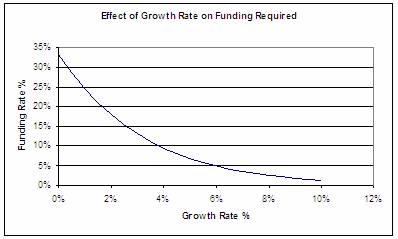

Sensitivity to interest and dividend rate

16. The (OVER OPTIMISTIC)

graph below illustrates the relationship between fund growth and the theoretical

level of funding. The figures behind the graph assume that the “Pension-Pot”

attracts the growth rate of interest for the whole of its life of 60 years that

is 40 years paying into the fund followed by forty years drawing a pension of

2/3rds of income. These figures do not take account of inflation and assumes

that income remains constant for the whole of ones working life and that the

“Pension Pot” is empty at the end of the 20 year pay-out period. In short,

the picture created in the graph below is far too rosy.

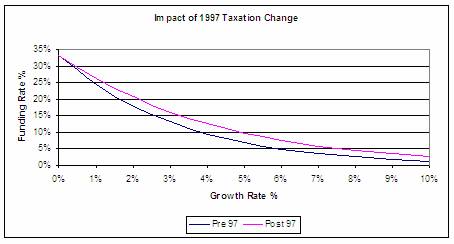

17. It is perhaps worth

referring to the impact of Chancellor Brown’s 1997, and each year since,

£5.3Billion raid on pension funds at this point. The 1997 change imposed

Corporation Tax on the payment of dividends into pension funds and for a pension

funds predominantly invested in

18. With reference to the

data contained in the graph above; if prior to the 1997 taxation change a 2/3rds

pension would be achieved if a pension fund had been funded at a rate of 9.5% of

Income with a 4% Growth Rate. Following the taxation changes it would have been

necessary to increase funding to 12.7% of Income, an increase of 3.2%, in order

to maintain the same level of Pension.

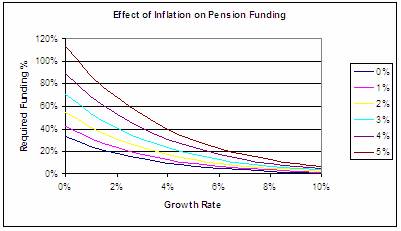

Effect of Inflation

19. The effect of

inflation is illustrated in the table and graphs shown below. As can be seen

from the table with a zero rate of growth and a 5% inflation rate, it would be

necessary to contribute 113% of income for a period of 40 yrs in order to fund

an inflation-proof (5%) for a period of 20 years. This is obviously not

possible.

|

PENSION FUNDING TO ACHIEVE 2/3rds FINAL SALARY

PENSION | ||||||

|

|

|

|

|

|

|

|

|

Growth |

I n f l a

t I o n R a t e | |||||

|

Rate |

0% |

1% |

2% |

3% |

4% |

5% |

|

0% |

33.3% |

41.8% |

54.6% |

70.3% |

89.6% |

113.0% |

|

1% |

24.6% |

31.4% |

41.3% |

53.8% |

69.1% |

87.9% |

|

2% |

18.0% |

23.3% |

31.0% |

40.8% |

53.0% |

68.0% |

|

3% |

13.2% |

17.2% |

23.2% |

30.7% |

40.3% |

52.2% |

|

4% |

9.5% |

12.7% |

17.2% |

23.0% |

30.4% |

39.8% |

|

5% |

6.9% |

9.2% |

12.6% |

17.1% |

22.9% |

30.2% |

|

6% |

4.9% |

6.7% |

9.3% |

12.6% |

17.0% |

22.7% |

|

7% |

3.5% |

4.9% |

6.8% |

9.3% |

12.6% |

17.0% |

|

8% |

2.5% |

3.5% |

4.9% |

6.8% |

9.3% |

12.6% |

|

9% |

1.8% |

2.5% |

3.5% |

4.9% |

6.8% |

9.3% |

|

10% |

1.3% |

1.8% |

2.6% |

3.6% |

5.0% |

6.9% |

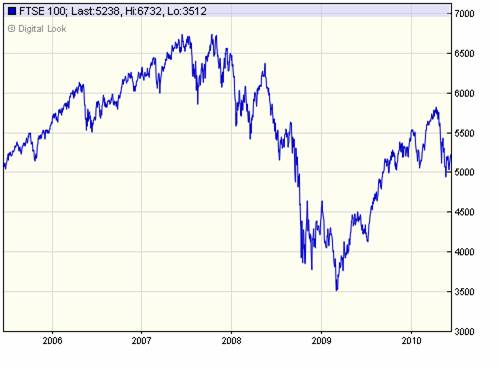

20. The conclusion to be

drawn from this table is that at current rates of growth (June 2010 with NatWest

deposit interest rates at 0.11%, Dividends at 4.13%, Increase in the value of

Stock Investments at 0% (see 5 year FTSE 100 Chart below – taken from

moneyweek.com web-site)) of 4% at best and inflation at 3% pension funding needs

to be at 23% of Income.

Conclusion

21. The conclusion from

the above is clearly that the adequacy of pension funding is dependant upon the

adequacy of the fund growth rate, and low rates of inflation. Life span is am

important element, but if growth rate was sufficient then the interest earned on

the “pension-pot” would be sufficient to meet all eventualities. The imposition

of dividend tax has had a significant effect on the pension process, resulting

in the system being unsustainable.

22. In assessing the

effect of Chancellor Brown’s 1997 pensions grab, the effect can be viewed

as:

- Reducing the income flowing from a “Pension-Pot” by 28%

- Necessitating a 39% increase in the size of the

“Pension-Pot” required to support the desired 2/3rds pension.

- Companies with defined benefits pension schemes are

forced to increase the funding to their schemes, resulting in the payment of

lower dividends, and

- A reduction in stock-market investment values.

- People with defined contribution-pensions are severely

impacted, as

- their capital base is lost as the value of the shares

which underpin their “Pension-Pot” declines, under the weight of defined

benefit schemes,

- growth rates are at least 28% lower than anticipated,

- their pension pot needs to be 39% higher than

anticipated,

- there is no way in which they can make personal

contributions out of earned income which would enable them to bridge this gap,

and the employers are under no obligation to make-good any shortfalls.